Cryptocurrencies like Bitcoin, Ether, Dogecoin, and countless others have been garnering more and more attention as the world eases out of lockdown. Over a year spent indoors has forced businesses to speed up digitization efforts. Thus, blockchain technology development started rising in popularity and some have begun to wonder if creating a cryptocurrency is a worthy endeavor.

As it turns out, it might be. According to research, the cryptocurrency market size is expected to reach $2.2 billion by 2026. What’s the leading force behind this? The need for transparency and distributed ledger technology.

If you’re looking to create your own cryptocurrency, you need to know what you are in for. Today, we will help you uncover what cryptocurrencies are, how they function, and how they are made. Moreover, we’ll talk about the pros and cons of cryptocurrency software development, and even discuss how much it may cost you. Let’s get started.

What is a Cryptocurrency?

The answer to the “what is a cryptocurrency” question will differ depending on who you ask. Some will tell you that it’s a new, digital form of money. Others will emphasize that it’s just another bubble, and the only thing driving it is media attention. At the end of the day, it’s up to you to decide. We’ll just focus on sharing information that’ll help you make the right choice.

Simply put, cryptocurrencies are digital assets that can be exchanged for goods and services. Typically, they are based on blockchain technology, with coin ownership records stored in a distributed ledger that uses cryptography to secure transactions.

There is, however, one nuance to discuss. Cryptocurrency development can mean one of the two things — coin or token creation. Both are cryptocurrencies, but there is one fundamental difference.

A coin operates on its own blockchain, while a token works on top of an existing one. For example, Bitcoin and Litecoin, as the names suggest, are coins, but Ether and Uniswap are tokens running on the Ethereum network.

Companies usually express more interest in tokens. That is because they can work like smart contracts and help startups get funding through a crowd sale. Additionally, they are easier and cheaper to create, but we will get into more detail about that later.

Discover the Key Things to Know About Smart Contracts Development

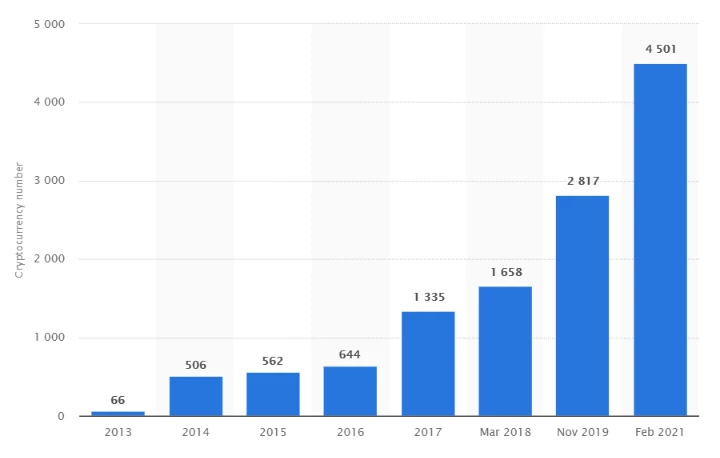

The number of cryptocurrencies worldwide is increasing every year. As of 2021, there are over 4,500, according to Statista. Since cryptocurrency creation isn’t too complex and blockchain development companies are widely providing this service, it’s no wonder there’s been a significant boost.

Currently, these are some of the most popular cryptocurrency examples:

- Bitcoin

- Ethereum

- Tether

- Litecoin

- Cardano

- Dogecoin

- Polkadot

- Uniswap

- Chainlink

- Monero

Whether you are hoping to eventually join these ranks or simply facilitate payments for your clients — learning how to create your own new cryptocurrency is essential. Hence, let’s take a look at how it all works.

How Cryptocurrencies Work

Distributed ledgers, which help cryptocurrencies operate, are built on consensus algorithms that regulate the addition of new blocks to the blockchain. Essentially, all network participants have to accept a block for it to register. Thus, these mechanisms serve as a way to confirm transactions that take place on the blockchain without involving a third party.

The two most popular consensus algorithms are Proof of Work (PoW) and Proof of Stake (PoS).

With PoW, a member has to prove to others that a specific amount of computational effort has been expended. This decentralized consensus mechanism got a lot of negative press lately. Primarily, due to its energy waste implications. It turns out, computers end up consuming a lot of electricity to perform computations with this consensus algorithm.

Source: Cambridge Bitcoin Electricity Consumption Index

PoS, on the other hand, doesn’t incentivize high energy consumption. Instead, it requires validators to stake their own Ethereum tokens to perform mining work, thus making them interested in reducing fraudulent activity on the network. Moreover, validators turn out to use much less computational power because they are selected at random and don’t compete with each other.

Cryptocurrencies are issued whenever a new block is created, and the blockchain participant has to be rewarded for validating the transaction through mining.

Find out how Velvetech helped build a secure Cryptocurrency Mining Browser

So, what does the process look like?

- Blockchain participant creates a transaction

- The transaction is broadcasted to a network of nodes

- The network validates the transaction

- A few transactions create a new block

- Blockchain participants, who allocated processing powers to validate the transaction, are rewarded with a cryptocurrency

Hopefully, you now have a better grasp of cryptocurrencies and how they work. However, to make an informed decision about the development of cryptocurrency, it’s best to know the pros and cons of the endeavor.

Pros and Cons of Cryptocurrency Development

Despite crypto dominating financial headlines, cryptocurrency development for business use is a less explored topic. Company leaders may be unsure of why creating cryptocurrencies should interest them. Hence, we want to share the benefits it can bring and a few things that may cause you to reconsider.

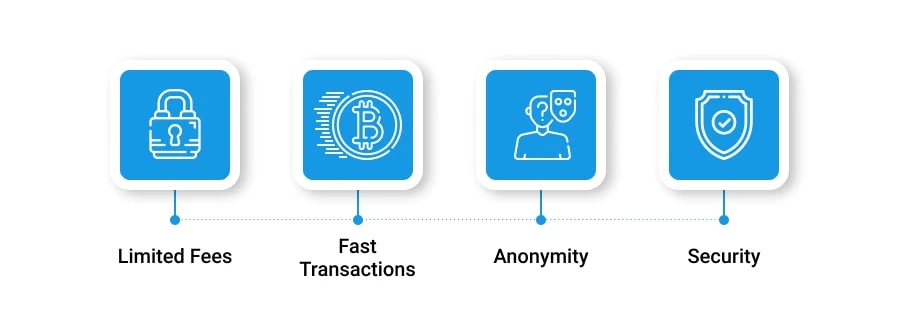

Cryptocurrency Advantages

Limited fees. Since cryptocurrencies eliminate the middleman, transaction fees are significantly reduced. You no longer have to pay for bank involvement like with fiat currencies. Of course, some fees are still required, but they are usually a lot lower than what we are used to with fiat transactions.

Fast transactions. With fewer intermediaries involved, the number of tasks needed to process the transaction is reduced. Hence, instead of waiting a couple of days to receive the money, the payment is quickly carried out to anyone with a crypto wallet.

Velvetech, a cryptocurrency wallet development company, can help build secure wallets for such transactions.

Anonymity. With crypto, purchases remain discreet and aren’t associated with a user’s personal data. Kind of like when you only use cash for a transaction. It’s hard to trace the money back to you. Sure, crypto isn’t completely anonymous or untraceable, but much less than traditional forms of payment.

Security. Advanced coding is involved in cryptocurrency transactions. They are encrypted, and the underlying blockchain technology verifies and secures the entire process, making it difficult to hack.

Cryptocurrency Disadvantages

Volatile value. As we have seen recently, cryptocurrencies are extremely volatile. Bitcoin’s annualized 30-day volatility reached 116.62% on May 24. The month started with the coin approaching the $60,000 mark, but in the second half of the month, it fell to around $31,000. Such drastic changes in value will make anyone skeptical and worried about the stability of the market.

Lack of regulation. Cryptocurrencies aren’t supported everywhere. Moreover, even in the United States where they are legal, there’s a lack of supervision. The technology is still in its nascent stage and regulators haven’t completely caught up to it. Hence, there can be some risks and roadblocks when you want to start your own cryptocurrency.

Irreversible transactions. Finally, the irreversibility of blockchain transactions can be concerning since any little mistake can cause you to lose funds. If you input an incorrect address — there’s no way to reverse the transaction, and your money might be lost.

How To Make Your Own Cryptocurrency

So, you want to create a cryptocurrency, but where do you start? Everything begins with getting clear about your goals. Why do you want to do it? How will cryptocurrency development help your business? Only after answering these questions can you get started.

In fact, it’s a good idea to compose a comprehensive white paper that describes your idea and all project aspects. However, let’s take a look at the high-level steps together.

1. Decide if You’re Making a Coin or a Token

First, you have to decide which development route you’re going to take. We’ve covered what the differences are between coins and tokens and now is the time to make a choice. Which one do you want to make?

Creating a coin is a more difficult option, and you’ll likely need a team of experienced professionals who provide cryptocurrency development services. Supporting and maintaining the functioning of a crypto coin also requires additional resources. However, if you choose to follow a custom development route — your software vendor will be able to handle these tasks.

Additionally, partnering with experts in cryptocurrency wallet development services can help you ensure users have a secure way to store and manage your new coin.

Token creation is usually more feasible for businesses to start. In this case, you’ll basically build a token on top of an existing, reliable blockchain.

Since tokens are what companies tend to go with when starting their cryptocurrency creation journeys, the next steps will relate to them in particular.

2. Pick a Blockchain Platform

After choosing to develop a token, you have to pick a blockchain platform on which it will be based. The choice depends on the consensus mechanism you want to have.

Most likely, the choice will fall on Ethereum due to its smart contract capabilities and DApp development facilitation. However, there are other popular solutions you can consider.

Here are some examples of other blockchain platforms:

- NEO

- EOS

- Waves

- Hyperledger Fabric

3. Code a Smart Contract and Create Your Token

Assuming you’ve chosen to go with Ethereum, the next step will be to deploy a smart contract on the network. ERC-20 is one of the most popular Ethereum tokens and is used for all smart contracts on the blockchain.

You’ll have to decide on the token amount, what it’ll be called, its symbol, and decimal places. Afterward, you’ll need to create a transfer event that will notify wallets when token transfers occur. Finally, after you’ve tested and verified your token it can be launched!

A lot of factors affect how the cryptocurrency creation process will look for you. Is a coin or a token the better choice for your business? Will you need to hold an ICO, or not? Each of the answers will modify the tasks involved in creation.

Uncover the 10 Steps of Launching a Successful ICO

Tech-savvy business leaders may ask themselves how to make a cryptocurrency, and the above steps provide a general overview. However, there are a lot of technicalities involved in cryptocurrency development. Hence, it’s always best to get a consultation on your unique business case and come up with a solution that will best suit your needs.

Cryptocurrency Development Costs

After answering the “how to make your own cryptocurrency” question, we think it’s important to talk about the cryptocurrency development budget.

We went over the high-level steps of cryptocurrency creation and used the more feasible token production process as an example. However, the development of coins, tokens, smart contracts, and everything else to do with the blockchain sphere requires a lot of technological know-how.

Of course, you can hire your own team, but the average blockchain developer salary reaches $107,000/year in the United States. Moreover, they aren’t so easy to come by, and having to spend time and money on headhunting is also something you have to consider.

If you choose to go with custom development services, expect developer hourly rates to vary depending on their experience and location. A $100/hour rate is common but can increase if the developer has worked on many successful blockchain projects.

Overall, custom software development costs are difficult to estimate precisely due to a variety of factors affecting them. The general range is anywhere between $5,000 to $1,000,000. We understand that this provides little clarity. However, if you can determine how many developers you will need — simply multiply the amount by their hourly or yearly rate, and you’ll get a rough approximation.

Starting Cryptocurrency Development

Now that you know how to create a cryptocurrency for yourself, you may be eager to start the journey. As you have seen, it’s not a very easy process. A lot of decisions are involved in the cryptocurrency development and technical difficulties can arise at any moment.

Moreover, the industry you operate in also plays a major role. Insurance blockchain development can somewhat differ from that of healthcare, for example. Hence, it’s imperative to have an experienced team at your side to facilitate the entire undertaking.

At Velvetech, we pride ourselves on a personalized approach with all our clients. We’ll be happy to help your company reach new heights with cryptocurrency development and guide you throughout the entire process. So, don’t hesitate to reach out to our team for a consultation and to discuss your innovative project.

About the author

Reach Out to Us